Managing your finances effectively is crucial for achieving long-term financial stability and growth. Avoiding common money mistakes can help you save more, invest wisely, and reduce financial stress. Here are five money mistakes to watch out for:

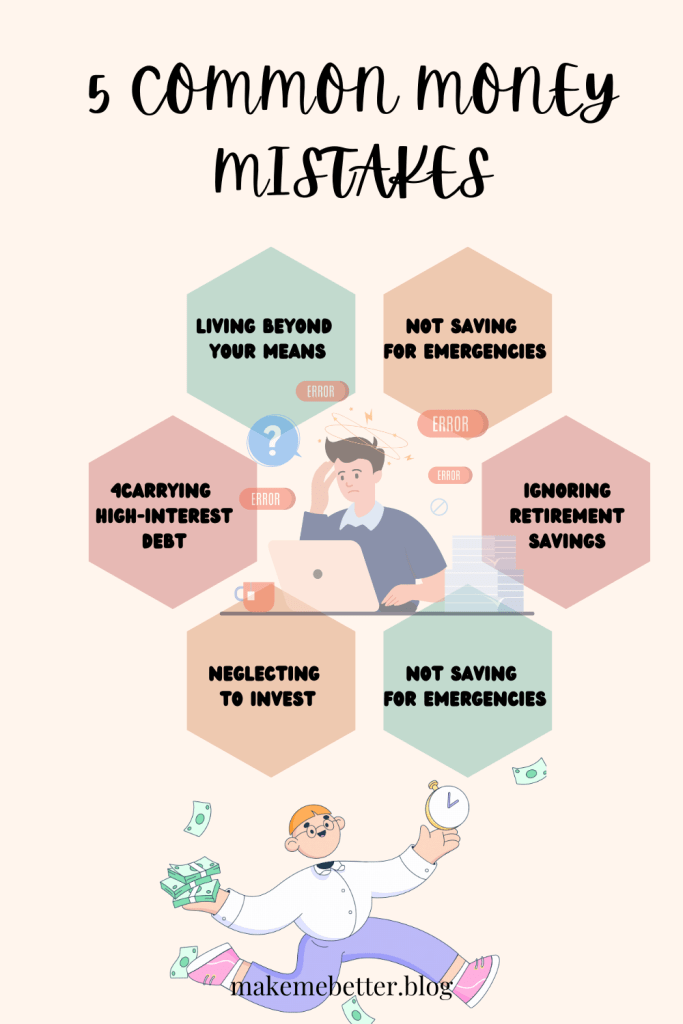

1. Living Beyond Your Means

One of the most common financial mistakes is spending more than you earn. This often leads to accumulating debt, which can be difficult to pay off. To avoid this, create a budget that tracks your income and expenses. Stick to your budget and prioritize saving over unnecessary spending. Consider using budgeting apps to help manage your finances more effectively.

2. Not Saving for Emergencies

Failing to build an emergency fund can leave you vulnerable to unexpected expenses, such as medical bills, car repairs, or job loss. Aim to save at least three to six months’ worth of living expenses in an easily accessible account. This safety net will provide financial security and peace of mind, allowing you to handle emergencies without going into debt.

3. Ignoring Retirement Savings

Procrastinating on retirement savings can jeopardize your financial future. The earlier you start saving for retirement, the more time your investments have to grow. Take advantage of employer-sponsored retirement plans, such as 401(k)s, and contribute enough to receive any matching funds. Additionally, consider opening an Individual Retirement Account (IRA) to supplement your retirement savings.

4. Carrying High-Interest Debt

High-interest debt, such as credit card debt, can quickly become overwhelming and hinder your ability to save and invest. Focus on paying off high-interest debts as soon as possible. Consider using the debt snowball method (paying off the smallest debts first) or the debt avalanche method (paying off the highest interest debts first) to tackle your debt effectively. Avoid taking on new high-interest debt by living within your means and using credit responsibly.

5. Neglecting to Invest

Keeping all your money in a savings account can limit your financial growth. While saving is important, investing is crucial for building wealth over time. Educate yourself about different investment options, such as stocks, bonds, mutual funds, and real estate. Start with low-cost index funds or exchange-traded funds (ETFs) if you’re new to investing. Diversify your investments to manage risk and maximize potential returns.

Avoiding these common money mistakes can significantly improve your financial health and set you on the path to long-term success. By living within your means, saving for emergencies and retirement, paying off high-interest debt, and investing wisely, you can achieve financial stability and growth. Take control of your finances today and make informed decisions to secure a prosperous future.

Leave a comment